Bank of Canada cuts 0.25% to 2.25%. Who benefits?

The Bank of Canada rate October 2025 annuncement delivered a 0.25% cut, bringing the overnight lending rate down to 2.25%. This change marks another step in the Bank’s gradual easing cycle and is already making an impact on mortgage rates, home affordability, and buyer sentiment. For Vaughan and GTA homeowners, the new rate could slightly reduce variable payments and improve qualifying conditions for upcoming renewals and new purchases.

BoC Policy Rate

2.25%

Prime Rate

4.45% (TD 4.60%)

Next BoC Meet

Dec 10, 2025

TL;DR (fast facts)

BoC policy rate: 2.25% (-0.25%)

- Prime rate: now about 4.45%; TD mortgage prime 4.60%

- Payment math (variable): ~$15/month per $100k cut for standard amortizations (25–30 yrs)

- Fixed rates: depend on 5-yr Government of Canada bond yields (≈2.6–2.75% lately)

- Why the cut: inflation easing toward target, softer growth & labour market, trade-policy headwinds ebbing

- Next BoC decision: Dec 10, 2025

This is the kind of home that adapts to your needs. Whether you’re growing a family, hybrid working, or just want a bit more elbow room — it ticks all the right boxes.

What changed—and why it matters

The Bank of Canada lowered the policy rate by 25 bps to 2.25%, setting the Bank Rate at 2.50% and deposit rate at 2.20%. The Bank signalled cuts are nearing an end unless the outlook shifts.

Context: headline CPI 2.4% in September (core still above 2%), GDP contracted −1.6% in Q2, unemployment around 7%, and tariff frictions easing at the margin.

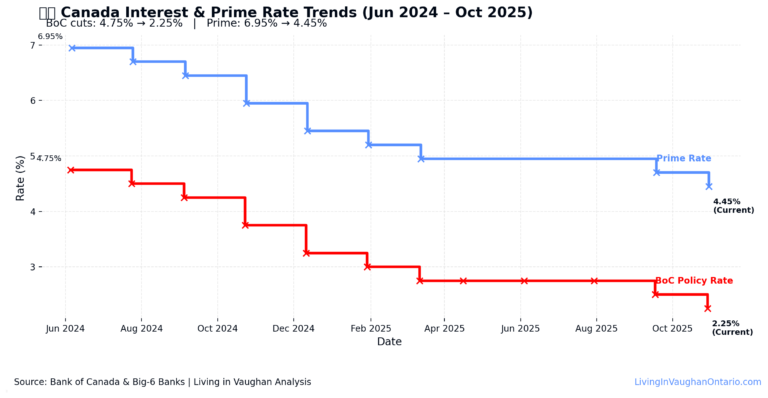

Prime Rate Trends

Canada’s key lending rates have both trended downward since mid-2024.

The Bank of Canada’s policy rate dropped from 4.75 % to 2.25 %, while major banks’ prime rate followed from 6.95 % to 4.45 %.

The narrowing gap shows how central-bank moves ripple directly into mortgage and credit costs across the GTA

Who actually benefits (and who doesn’t)

With the Bank of Canada interest rate October 2025 now at 2.25%, variable-rate borrowers will notice immediate relief: anyone with variable-rate mortgages, HELOCs, or variable business loans (they’re priced off prime).

Big lenders moved prime to ≈4.45% (TD mortgage prime 4.60%).

How much relief?

Payment change for a 0.25% cut ≈ $15/month per $100k of mortgage (25–30-year amortization).

Examples:

- $500k variable → save ~$75/month

- $800k variable → save ~$120/month

(Back-of-napkin aligns with amortization math; not advice—ask your broker for your exact numbers.)

Who may not feel it yet

Fixed-rate borrowers: Your rate follows 5-year GoC bond yields. Those yields hovered ~2.6–2.75% around the announcement; if they dip, lenders may trim fixed rates—but bond moves, not BoC, drive that.

Groceries & essentials: Policy rate tweaks demand, not supply. Food prices track supply chains more than BoC moves.

What’s next for Vaughan & GTA real estate?

This Bank of Canada rate October 2025 update is part of a broader easing trend that began earlier this year

Buyers: Slightly better affordability for variables; pre-approvals may stretch a touch farther. Watch bond yields for fixed-rate quotes

Sellers: Lower rates can nudge showings up in rate-sensitive segments (towns/condos, entry-detached). Pricing still needs to reflect local comps & inventory.

Investors: Cap rates and debt costs are inching closer; underwriting still needs conservative rents/vacancy.

Renewals (2025–2026): If you’re within 6–12 months, compare blend-and-extend vs. switch vs. shorter terms. A broker can model total interest & penalties.

Smart next steps (no fluff)

- Renewal in 6–12 months: Ask for a rate hold and a switch-vs-refi comparison

- Buying soon: Get both fixed and variable quotes; stress-test at +2% to be safe

- HELOC strategy: Consider splitting: portion fixed, portion variable for flexibility

- Book a 15-min call: I’ll connect you directly to my mortgage broker for tailored options

Ready for a no-pressure plan?

Book a call – Take advantage of this Bank of Canada rate October 2025 update

I’ll introduce you to my mortgage broker to provide custom / specific comps that matter to YOU!

As the Bank of Canada rate October 2025 continues to guide mortgage trends, staying informed can help buyers and sellers plan smarter.

Ready for a no-pressure plan?

Sources (key links)

- Bank of Canada press release: policy rate 2.25%, Bank/Deposit rates; next decision Dec 10, 2025.

- StatsCan CPI (Sept 2025): headline 2.4%; details on components.

- Prime rate changes: Big-Six prime to 4.45%; TD mortgage prime 4.60%.

- 5-year GoC bond yield context (drivers of fixed rates)

- Macro backdrop (GDP –1.6% Q2; labour softening; tariff context).

Learn all about Vaughan!

📅 Book Free Consultation

Should you buy a home yet?

Let’s talk.

📲 Call or Text Me Directly